-

19 min read

Mar 12, 2026 3:51:09 PM

Share On:

What Actually Happens With Taxes, IRAs, Roth IRAs, Solo 401k Plans, and UBTI

Retirement capital is flowing into private real estate at record levels.

Self-directed IRAs are more common. More professionals have consulting or side-business income. Most multifamily syndications use leverage.

That combination creates opportunity.

It also creates structural tax consequences that many investors do not fully understand.

One of the most common assumptions we hear is:

“If I invest through my IRA or Roth, taxes do not matter until I withdraw.”

Sometimes that is true.

In leveraged real estate, it often is not.

This is your clear, strategic framework for understanding what actually happens, where UBTI fits, why Solo 401k plans are treated differently, and how sophisticated investors structure retirement capital intentionally.

This article is educational only. Investors should consult their CPA, tax advisor, or retirement plan specialist regarding their specific situation.

Key Takeaways for Sophisticated Retirement Investors

• IRAs and Roth IRAs can owe tax on leveraged real estate through UBTI

• UBTI is a current-year compliance regime, not a deferred retirement tax

• If required, Form 990-T is filed for the retirement account and tax is paid from the account

• Bonus depreciation does not automatically eliminate UBTI exposure

• Solo 401k plans are generally exempt from UBTI on debt-financed real estate

• Account structure is a portfolio decision, not an afterthought

Why This Matters More Today

In today’s market environment:

• Multifamily investments frequently rely on leverage

• Accredited investors are increasingly seeking private alternatives

• Self-employment and 1099 income are more common than ever

• More investors qualify for Solo 401k plans

As private real estate becomes more mainstream among high-income professionals, retirement account structure is no longer a technical footnote.

It is part of portfolio architecture.

The Mental Model Most Investors Start With

Consider a high-income professional.

She has:

• A rollover Traditional IRA from a prior employer

• An actively funded Roth IRA

• A consulting business generating side income

She wants passive exposure to multifamily real estate.

Her assumption is logical:

“Retirement accounts grow tax deferred or tax free. So taxes do not apply until retirement.”

That assumption works well for:

• Stocks

• Bonds

• Mutual funds

• ETFs

It becomes incomplete when the investment uses debt.

To understand why, we need to understand UBTI.

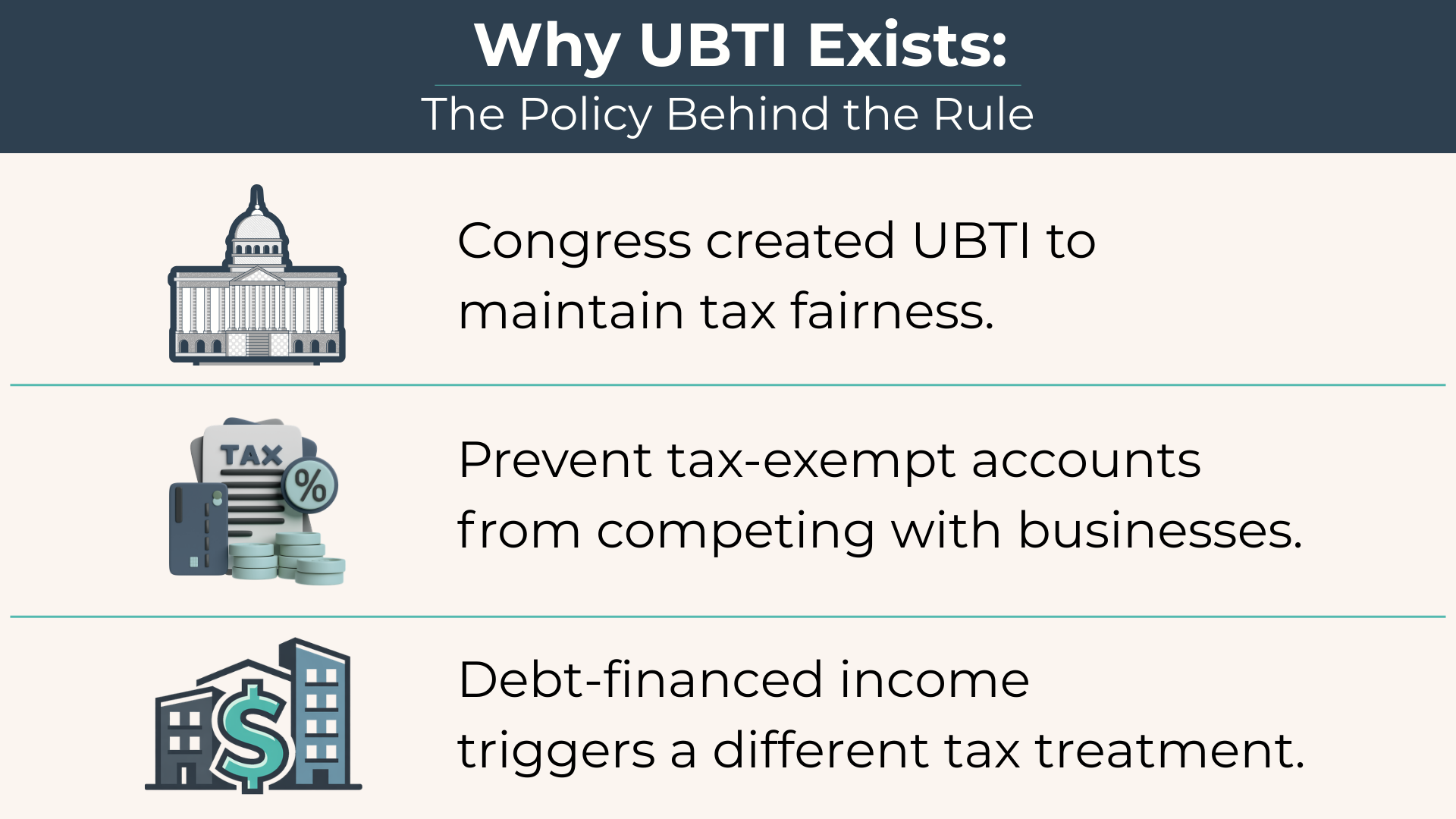

Why UBTI Exists in the First Place

UBTI stands for Unrelated Business Taxable Income.

The concept was created to prevent tax-exempt entities from competing unfairly with taxable businesses.

Congress did not intend retirement accounts and charities to operate active businesses without tax consequences.

When a retirement account earns income that resembles operating income from a business, the IRS may treat it differently.

Real estate introduces a unique twist.

When a property is financed with debt, a portion of the income is considered debt-financed income. For IRAs and Roth IRAs, that portion can create UBTI.

This is not about punishing retirement investors.

It is about maintaining parity between tax-exempt capital and taxable business activity.

The important shift:

UBTI is not a future retirement tax.

It is a current-year filing regime.

How Leverage Triggers UBTI in Real Estate Syndications

Most multifamily syndications use financing.

Debt amplifies purchasing power.

Debt can enhance returns.

Debt is standard in commercial real estate.

However, from a retirement account perspective, the portion of income attributable to borrowed funds may be treated as Unrelated Debt-Financed Income.

That income flows into UBTI calculations for IRAs and Roth IRAs.

If UBTI exceeds the applicable IRS threshold in a given year, the retirement account may:

• Be required to file Form 990-T

• Owe tax at trust tax rates

• Pay that tax from within the account

This is where expectations and reality often diverge.

What Actually Happens Each Year: The Practical Mechanics

Let us walk through the process.

Step 1: The syndication issues a Schedule K-1.

If UBTI exists, it is disclosed within the K-1 reporting or supporting statements.

Step 2: The investor provides the K-1 to the custodian or CPA.

Many custodians do not automatically receive or process this information without investor direction.

Step 3: UBTI is calculated at the account level.

If the retirement account holds multiple investments generating UBTI, the amounts may aggregate.

Step 4: If required, Form 990-T is prepared and filed on behalf of the retirement account.

Step 5: Any tax due is paid from the IRA or Roth balance.

The investor does not pay personally.

The account pays.

An important practical consideration:

The retirement account must have sufficient liquidity to cover any tax due. If all capital is tied up in illiquid investments, paying tax can become administratively complicated.

This is rarely discussed. It matters.

Sponsors provide UBTI reporting information.

They do not file 990-T for investors.

Responsibility ultimately rests with the account holder and their service providers.

The Critical Structural Exception: Solo 401k Plans

Here is where the conversation becomes strategic rather than purely technical.

While IRAs and Roth IRAs can be subject to UBTI from leveraged real estate, Solo 401k plans are generally treated differently under current tax law.

Qualified employer plans, including Solo 401k plans, are typically exempt from UBTI related to debt-financed real estate under Internal Revenue Code Section 514.

This is not a minor distinction.

It can materially change compounding outcomes.

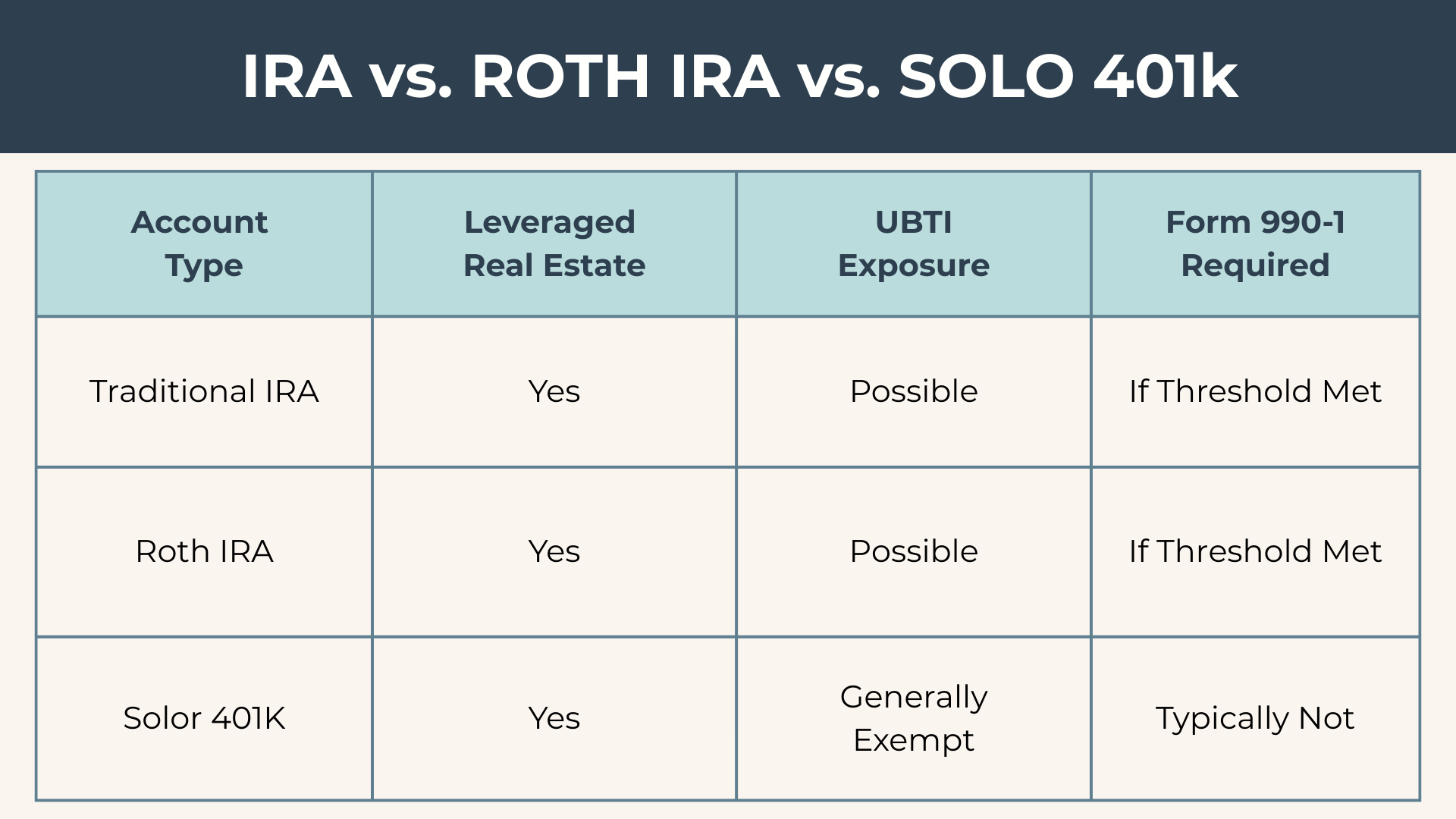

What That Means in Practice

If leveraged real estate is held inside:

Traditional IRA - UBTI is possible

Roth IRA - UBTI is possible

Solo 401k - UBTI from real estate leverage is generally exempt

In many cases, this means:

• No Form 990-T solely due to leverage

• No current-year UBTI tax friction

• Cleaner internal compounding

It is important to note:

The exemption generally applies to debt-financed real estate. It does not automatically apply to all operating business activities.

Structure still matters.

Why Solo 401k Plans Are Treated Differently

Congress historically treated employer-sponsored retirement plans differently than individual retirement accounts.

401k plans were designed as employer-based retirement vehicles.

As a result, they receive more favorable treatment in certain areas, including debt-financed real estate.

IRAs, while powerful, do not receive the same exemption under UBTI rules.

This distinction is structural, not arbitrary.

How Sophisticated Investors Align Account Structure With Asset Type

Returning to our earlier example.

Our investor has:

• A Roth IRA

• A rollover IRA

• Active self-employment income

Instead of placing leveraged multifamily investments inside her IRA, she:

Uses IRAs for liquid market exposure.

Establishes a Solo 401k for private real estate.

The result:

Her market investments grow within IRA structures.

Her leveraged real estate compounds inside a structure generally exempt from UBTI on debt.

Both accounts remain compliant.

Both serve distinct strategic roles.

This is not about eliminating tax.

It is about aligning the right vehicle with the right asset.

Eligibility and Structural Considerations for Solo 401k Plans

Solo 401k plans are generally available to:

• Self-employed individuals

• Business owners with no full-time employees other than a spouse

• Independent contractors

• Individuals with qualifying side-business income

Eligibility depends on earned income and business structure.

Not all Solo 401k plans permit alternative investments.

Before investing in syndications, investors should confirm:

• The plan allows private real estate

• The plan documents support alternative assets

• Administrative support is available

• The plan is properly established before funding investments

Account setup should precede allocation decisions.

Bonus Depreciation and Where Assumptions Fail

Many real estate investors assume:

“Bonus depreciation will eliminate UBTI.”

That assumption is incomplete.

Retirement accounts do not always benefit from depreciation in the same way taxable investors do. In some situations, depreciation used in UBTI calculations may be recomputed under different rules.

Bonus depreciation can significantly reduce taxable income in personal accounts.

It does not automatically eliminate UBTI exposure inside IRAs.

The “IRS Does Not Really Care” Misconception

Some investors reason:

“If I miss something, the IRS benefits.”

That logic does not apply here.

UBTI is a current-year filing requirement.

Failing to report required UBTI is not a matter of overpaying later. It may mean underreporting taxable income now.

For Roth IRAs, this is particularly important.

Because qualified withdrawals can be tax free, UBTI may be one of the only times tax applies.

Compliance should be intentional.

Investor Checklist Before Using Retirement Capital in Real Estate

Before investing through a retirement account, ask:

Does this deal use leverage

If using an IRA or Roth, could UBTI apply

Would a Solo 401k structure change tax treatment

Will UBTI reporting information be provided annually

Who prepares Form 990-T

Does my account have liquidity for potential tax payments

How does this investment interact with other retirement holdings

Five informed questions can prevent years of avoidable friction.

Frequently Asked Questions

Does a self-directed IRA owe taxes on leveraged real estate?

It can. If debt-financed income creates UBTI above the annual threshold, the IRA may owe tax and require Form 990-T.

Does a Roth IRA pay UBTI on real estate?

Yes. Roth IRAs can be subject to UBTI when investing in leveraged real estate.

Can UBTI from multiple investments be combined?

Yes. UBTI is calculated at the account level, so multiple investments within the same IRA may aggregate.

Are Solo 401k plans subject to UBTI on leveraged property?

Under current tax law, qualified employer plans such as Solo 401k plans are generally exempt from UBTI related to debt-financed real estate.

Should I change account structures before investing?

Structural decisions depend on eligibility, income, and long-term planning. Investors should consult a CPA or qualified retirement plan provider before making changes.

Educational Resources for Retirement Account Investors

Investors exploring self-directed retirement structures often consult:

• Self-directed IRA custodians that support alternative investments

• Solo 401k plan providers that allow private real estate

• CPAs experienced with Form 990-T filings

Quattro does not endorse specific providers and does not provide tax advice.

We do provide UBTI reporting information for retirement investors so they can work effectively with custodians and advisors.

Why This Matters Now

Private real estate continues to attract retirement capital.

Leverage remains standard in multifamily investing.

At the same time, more accredited investors qualify for Solo 401k plans due to entrepreneurial and consulting income.

Retirement accounts are powerful.

They are not identical.

Sophisticated investors think beyond the deal.

They think about structure.

They think about compounding efficiency.

They think about compliance before the K-1 arrives.

When account structure aligns with asset type, capital compounds with fewer surprises and greater clarity.

That is not complexity.

That is intentional portfolio design.

.png)

.png)

The Quattro Team is passionate about helping investors achieve financial freedom through smart asset backed investments. We combine deep market knowledge with a people-first approach to create wealth and impact for our partners and communities.

Comments